The Balance Sheet

We’ve talked about the income statement and the cash flow statement in this series. Now let’s talk about the balance sheet. It provides us with an overview of what the company owns and owes, along with what kind of equity the shareholders have in the company for the accounting period. (All the pictures in the article are from the financial report for Hindustan Aeronautics Ltd for FY 2022)

So, the balance sheet has 3 major components: Assets, Liabilities and Shareholders’ Equity. And you need to remember this equation:

Assets = Liabilities + Shareholders’ Equity

Shareholders’ Equity refers to the shareholders’/owners’ wealth in the company. The “wealth” term is counterintuitive here, but since the company is an entity of its own, we can remember this money as whatever is owed by the company to its owners. It includes Share Capital (Face Value of all outstanding shares) and Reserves & Surplus (Reserves are funds set aside for specific purposes in the future and surplus is simply the extra profit that the company saves in its coffers).

Coming to the liabilities listed on the balance sheet. The first entry is for the non-current liabilities, which are the liabilities that are to be settled in more than a year’s time. This category mainly includes long-term borrowings, provisions (generally funds set aside for employee benefits, etc.), and deferred tax liabilities.

The next one is current liabilities, and these are to be settled within 365 days. These mainly include short-term borrowings, trade payables and short-term provisions.

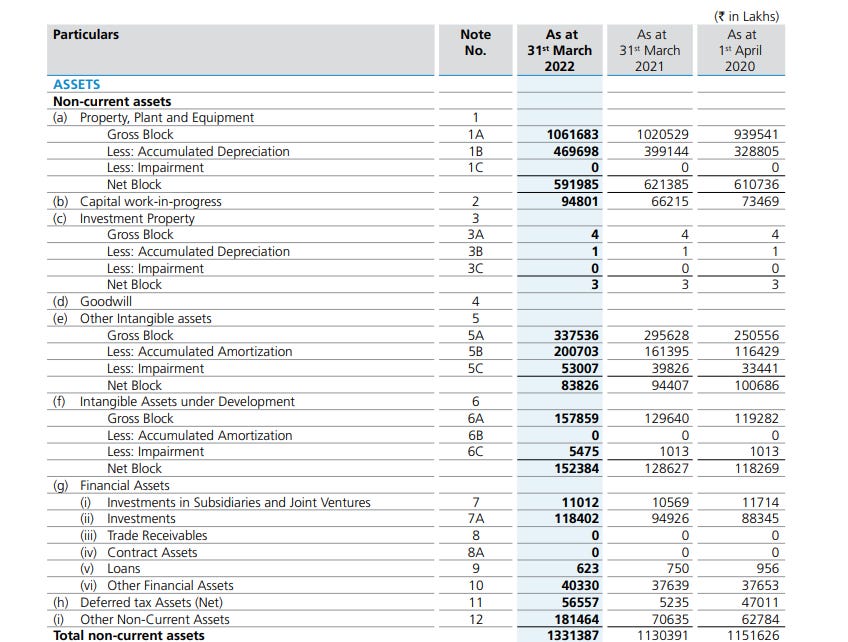

Let’s look at the asset side of the balance sheet. This is also divided into non-current assets and current assets, and the time frame to differentiate between these two is the same as liabilities - 365 days. Non-current assets include physical assets (factories, offices, etc), intangible assets (patents, copyrights, etc.), capital work in progress (assets under construction) and intangible assets under development (patent filing, ad development, etc.).

Current assets include inventory, account receivables (money which is owed to the company by its customers and others), cash and cash equivalents, and short-term loans that the company has given out.

Now that we’ve talked about all three types of financial statements a public company provides to the market, we’ll look at how to analyse these statements using some financial ratios in a later article. Meanwhile, you can more articles from me here. And do let me know if you want a specific topic covered! Subscribe for free to receive more posts like this every day!